The Wine On Premise UK 2025 report is a bit like a wine list in itself - designed to help those using it find what they are looking for. From revelaing who the best distributors are to work with, to what are the most listed wine brands and styles, to what prices are being charged by the bottle or glass. Here we examine which countries and regions are most in demand and what you might have to pay to buy their wines. Peter McAtamney reports.

Spain and Portugal

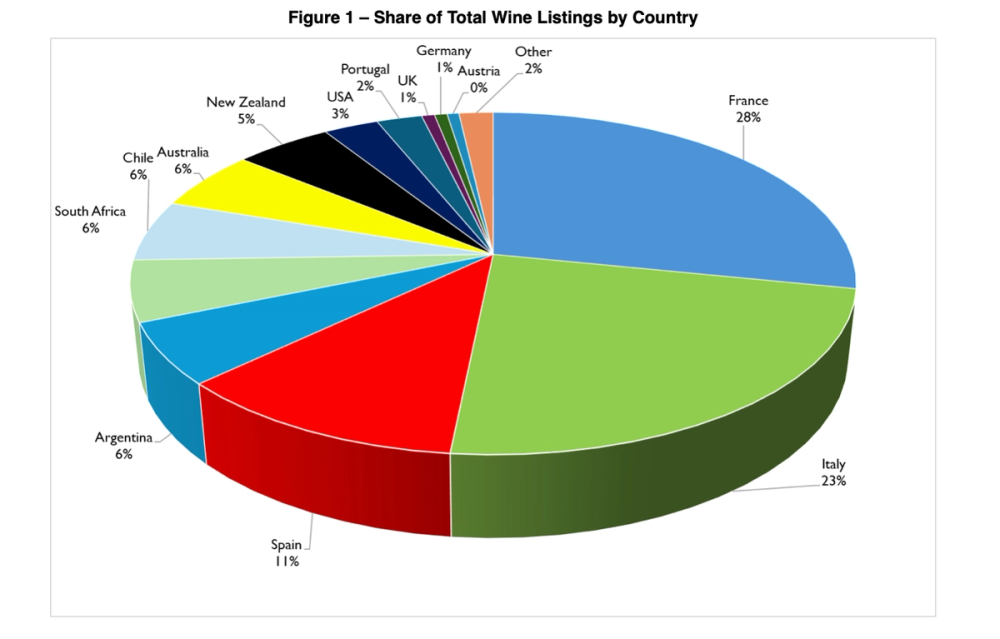

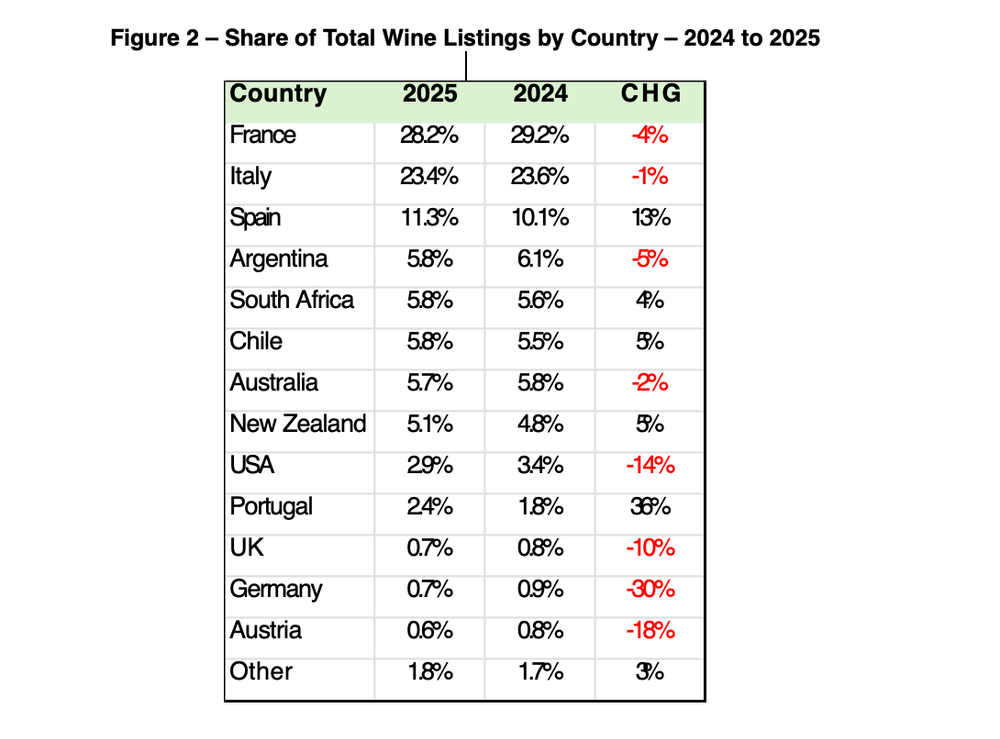

Spain and Portugal have been the most successful countries in terms of growing their share of listings on UK wine lists during the last 12 months. Spain’s success comes down to two factors.

Firstly, a growing awareness of the white wines of northern Spain. This includes a big upsurge in listings of Viura (also known as Macabeo in Catalonia) driven blends out of Rioja, as well as Verdejo from Rueda and Castilla y Leon and Godello-based wines from across the northwest of Spain.

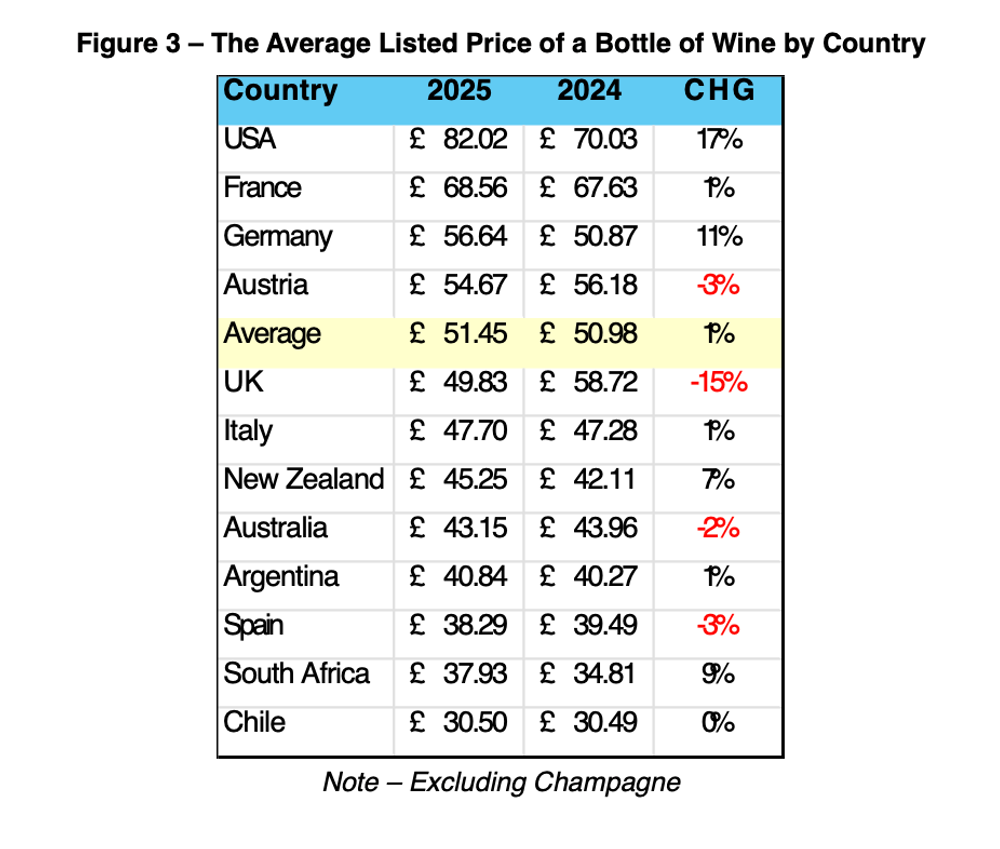

Secondly, cheaper red wines of La Mancha and surrounding DOs. This won't necessarily help Spain’s image and is proving a drag on average prices achieved.

For Portugal, the Minho region has had a significant lift in listings, also due to increased awareness and preference for the white wines of the Northern Iberian Peninsula. Anyone attending Wine Paris, for example, could not have missed the huge presence of the winemakers of Vinho Verde.

France

France lost the most listings of the three major wine-producing countries but will almost certainly recover these as the market picks up again. It always does. Both Champagne and Bordeaux increased listings despite the troubles both regions are facing, more broadly.

Italy

Italy is more or less stable, overall. There has been a significant drop in listings of Prosecco, which is tending to be replaced by French Crémant and in listings of cheaper Pinot Grigio. Regions such as Marche, Emilia-Romagna, Abruzzo and Sicily are, however, attracting more attention as are the red wines of the Veneto.

Argentina and Chile

Argentina seems to have finally hit a peak, but you can never count Argentina out. Malbec is still the most listed red wine style on UK wine lists and Mendoza, the most listed red wine source.

Chile saw its listings increase but at prices that are now well adrift of the rest of the market.

South Africa and New Zealand

South Africa is in the zone particularly where its white wines are concerned. They and New Zealand are the only New World wine-producing countries to have increased their share of listings whilst steadily increasing prices.

Australia

Australia continues its long-term decline with few lessons having been learnt about how to play in this or any other international on-trade market.

The US

The US is the fastest declining of the New World producer countries. Strong currency, near-prohibitive prices at the top end and too many listings at the bottom make the UK a tough market for the medium-sized US producers who need to be well-represented here for the category to succeed.

The UK

The UK industry is flying backwards just when listings need to be rapidly increasing. If you take out Chapel Down and table wine producers, English sparkling wine, seen alone, is in a precarious position.

Austria and Germany

After a very strong run in recent years, the market seems to have turned its attention away from the more aromatic wines including those of Austrian and German wines. One of the great mysteries of this market is why German Riesling, particularly, and Riesling more broadly remains so underrepresented. Australian Riesling (Clare Valley), at least, is growing a fan base.

Pricing

Prices, overall, are unchanged from a year ago after a period of significant inflation, meaning that the average consumer may be drinking worse wine after absorption of excise duty increases and other increased costs. Restaurants and their suppliers are, however, getting ever more resourceful, in terms of seeking out value across the wine world.

Note – Excluding Champagne

* You can find more insights from Wine Business Solutions here.

* To find out more and order the Wine On-Premise UK 2025 report click here.